Why Outfitters Should Stop Using Venmo for Deposits

You send a Venmo request for $1,500. The hunter pays it. The memo line says "duck hunt." Six months later, opening weekend rolls around and the hunter doesn't show. No call, no text, just gone.

You kept a spot open all season. You turned other hunters away. And now you're staring at a Venmo transaction with zero terms, zero cancellation policy, and zero recourse. The $1,500 you collected doesn't come close to covering what that empty blind cost you.

This happens to outfitters and fishing guides every single season. And most of the time, the payment tool is the root of the problem.

The real problems with Venmo and Cash App for outfitter deposits#

Venmo, Cash App, and Zelle were built for splitting dinner tabs and paying your buddy back for gas. They were not designed to run a booking operation. When you use them to collect deposits from clients, you're introducing risk into every transaction.

No invoice, no paper trail

A Venmo payment is just a dollar amount with an optional memo. There's no line-item breakdown, no terms of service, no cancellation policy, and no formal record that ties the payment to a specific trip on a specific date. If a dispute comes up, you have nothing to point to except a transaction that says "fishing trip."

Zero chargeback protection

Most outfitters use personal Venmo accounts, which offer essentially no seller protection. Even Venmo business accounts have limited coverage, and the dispute process is stacked against sellers. If a hunter files a chargeback through their bank, you're almost guaranteed to lose that money. Compare that to a proper payment processor like Stripe, where documented invoices with signed terms give you real evidence to fight disputes.

No deposit terms or cancellation policy

When a hunter sends you $1,500 on Venmo, what did they agree to? Can they cancel for a full refund? Is the deposit non-refundable after 30 days? What happens if they no-show? None of that is captured in the transaction. You might have a policy, but if it's not attached to the payment, it doesn't exist in any enforceable way.

It looks unprofessional

Hunters are spending $2,000 to $10,000 on guided trips. They're comparing outfitters, reading reviews, and evaluating who runs a tight operation. When one outfitter sends a Venmo request and another sends a professional invoice with itemized pricing and clear terms, the second outfitter looks like the safer bet. First impressions matter, and your payment process is one of the first things a client experiences after booking.

No automatic receipts or confirmations

After a hunter pays via Venmo, what happens next? In most cases, nothing. The hunter has no confirmation of what they booked, when the trip is, or what the remaining balance looks like. That means more texts, more back-and-forth, and more opportunities for miscommunication.

Tax tracking is a nightmare

At year end, you're scrolling through hundreds of Venmo transactions trying to figure out which ones were deposits, which were final payments, and which were your buddy paying you back for bait. Reconciling informal payment apps with your actual bookings is time you'll never get back.

Limited payment methods

Not every hunter wants to pay through Venmo. Some prefer to use a credit card for the points. Others want to pay via bank transfer to avoid processing fees. Venmo limits you to one payment rail, which means you're either turning away bookings or managing multiple payment methods across multiple apps.

What "good enough" is actually costing you#

Here's where most outfitters get stuck. Venmo works. Deposits come in. Trips happen. So why change anything?

Because "good enough" has a real dollar cost that most outfitters don't calculate.

The no-show math

If 15 to 20 percent of your informal bookings cancel late or no-show without penalty, and your average trip runs $3,000, the numbers add up fast. On a 10-booking season, that's $4,500 to $6,000 in lost revenue. For guides running 30, 40, or 50+ trips a year, the losses are significantly higher.

A non-refundable deposit with clear cancellation terms attached to every payment dramatically reduces no-show rates. But those terms only work if they're part of the transaction, not in a text message you sent three months ago.

The professionalism gap

Hunters talk. They compare experiences. The outfitter who sends a clean invoice with their logo, itemized pricing, and a secure payment link stands out from the one who texts a Venmo handle. If you're competing for repeat clients and referrals, your payment process is part of your brand.

The time cost

How many hours do you spend each month chasing late payments, sending reminders, and manually tracking who paid what? How much time do you lose at tax time reconciling a year's worth of Venmo transactions? That's time you could spend scouting, marketing, or just being in the field. For most outfitters, switching to proper invoicing saves three to five hours per month in administrative work.

Track your no-shows and late cancellations for one season. Multiply by your average trip price. That number is the real cost of not having enforceable deposit terms.

What professional payment collection actually looks like#

Professional deposit collection isn't complicated. It's just structured. Here's what it looks like in practice.

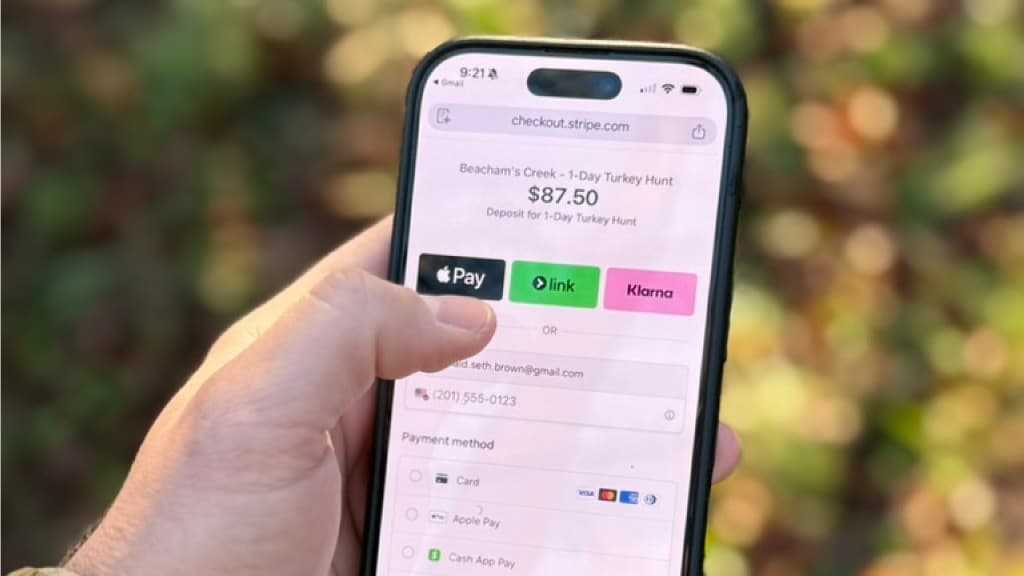

A real invoice with itemized pricing. Your client sees exactly what they're paying for. Trip dates, species, number of hunters, lodging, meals, whatever your package includes. No ambiguity.

A branded payment page. When a hunter clicks "Pay," they see your operation's name and logo, not a third-party app. This reinforces trust and makes the transaction feel intentional.

Deposit terms and cancellation policy baked in. Before a hunter completes payment, they acknowledge your terms. This turns a casual money transfer into a binding agreement. If they no-show or cancel late, you have documentation.

Automatic receipts and booking confirmations. The moment payment clears, your client gets a receipt with trip details. No extra texts. No follow-up needed.

Calendar sync. The trip shows up on both your calendar and your client's. Fewer missed dates, fewer scheduling mix-ups.

Stripe-powered checkout. Cards, bank transfers, Apple Pay, Google Pay. Your clients pay however they want, through a PCI-compliant, bank-level secure payment page. You don't touch their card numbers.

This is what hunters expect when they're booking a $5,000 guided trip. It's also what protects you when things go sideways.

Professional invoicing built for outfitters

Acre lets you create and send a professional invoice from your phone in under 60 seconds. Branded payment pages, deposit terms, calendar sync, and Stripe-powered checkout included.

See How It Works"But my hunters prefer Venmo"#

This is the most common objection, and it doesn't hold up.

Hunters don't prefer Venmo. They use whatever you send them. If you send a Venmo request, they pay on Venmo. If you send a professional invoice link, they click it and pay. The friction is identical. In most cases, paying through an invoice link is actually easier because there's no app to download and no account to create.

Think about how you pay for things. When a contractor sends you an invoice link, you click it and pay with your card. You don't call them and ask if you can Venmo them instead. Your hunters are the same way.

Here's the part nobody talks about: the hunters who push back hardest on professional payment methods are often the ones most likely to cancel or no-show. A structured deposit process acts as a filter. Serious hunters don't blink at a professional invoice. The ones who balk at basic terms are telling you something about how they'll handle the rest of the booking.

The deposit process isn't just about collecting money. It's a signal. It sets the tone for the entire client relationship.

What to look for in a payment tool#

Not every invoicing tool is built for outfitters. Most are designed for contractors, freelancers, or e-commerce. Here's what actually matters for guides and outfitters.

Mobile-first

You're booking trips from a boat ramp, a truck, or a blind. Your payment tool needs to work from your phone without fumbling through a desktop interface. If you can't create and send an invoice in under two minutes from your phone, it's the wrong tool.

Deposit and balance payment support

Guided trips typically involve a deposit upfront and a balance due before or after the trip. Your tool should handle split payments natively, not force you to create two separate invoices or track balances manually.

Clear terms attached to every payment

Cancellation policies, refund terms, trip details. All of it should be visible to the client before they pay. This is what protects you in a dispute and what reduces no-shows in the first place.

Calendar integration

When a hunter books, that trip should automatically show up on your calendar. Bonus if it shows up on theirs too. This eliminates the back-and-forth scheduling that eats up time between booking and trip day.

Stripe-powered payments

Stripe is the industry standard for payment processing. It's what major platforms use. It accepts every payment method your clients want to use, and it gives you real dispute protection with documented evidence. If your booking software doesn't run on Stripe, ask why.

Making the switch#

You don't need to overhaul your entire operation overnight. You don't need to migrate old bookings or change how you communicate with clients. The switch is simpler than most outfitters expect.

Start with your next booking. Instead of sending a Venmo request, send a professional invoice. Include your trip details, deposit amount, cancellation policy, and a secure payment link. That's it.

Tools like Acre are built specifically for this. You can create and send a professional invoice from your phone in under 60 seconds. Your client gets a branded payment page, clear terms, and an automatic receipt. You get a documented booking with enforceable deposit terms and a calendar entry.

The difference between "we've always done it this way" and "we run a professional operation" is smaller than you think. It's one invoice.

Acre's Starter plan is free with no monthly fee. You only pay a small processing fee when you get paid. There's no commitment and no contracts to sign.

Your hunts are professional. Your payment process should be too.#

You invest real time and money into running quality trips. Your gear is dialed. Your land or water access is locked in. Your clients have a great experience in the field.

The payment process is the first and last touchpoint your client has with your business. It's worth getting right. Not because it's complicated, but because the alternative is costing you money, time, and credibility every season.

Your next booking is the right time to make the switch.